Our solar conundrum

PUBLISHED

May 03, 2026

KARACHI:

With the energy shock becoming more pronounced worldwide, consumption bills soaring, and a broad but fragmented consensus against fossil fuels shaping up, a growing chorus in the global north backs a shift to greener power. In the global south, however, many people are arriving at the same conclusion, not necessarily out of environmental concern, but for the sake of their wallets. Pakistan happens to be no exception. The thought of transitioning to solar crosses countless minds. Some can afford it, others can only afford to shelve the idea until they save enough, or until the country’s policy climate turns more conducive.

Asad, a resident of Karachi, the southern port city where the sun rarely hides, is one of those who has thought about it. Over the past few months, particularly as the energy shock continues to hammer consumers, he has sat at his table innumerable times, running a set of numbers he scribbled on a piece of paper. The math has always been simple, but the action wasn’t, not for someone watching every rupee, with no buffer for risk. With tariffs rising and load-shedding becoming the new normal, the decision felt almost obvious, the payback period made sense, and the long-term savings made even more sense. While he was convinced he would go ahead with the transition, when he actually decided to make the move, the realities around it had shifted beyond his reach.

The net metering regime he had based his calculation on had shifted to net billing. The already minimal buyback rate for excess electricity was now significantly lower, in some cases less than a third of the previous rate. The financial logic that once made the investment attractive no longer held. Instead of placing an order, Asad found himself pausing, recalculating, and reconsidering.

His situation reflects a growing uncertainty among consumers who, until recently, were at the centre of Pakistan’s solar uptake. Upper middle-income households like his can still afford the upfront cost, but policy changes have begun to alter the incentives that once drove adoption. Beyond this group lies a much larger segment that faces the same pressures — rising electricity tariffs, increasing fuel prices, and unreliable supply — but remains locked out of the transition altogether.

Over the past few years, solar has started to pick up across Pakistan. According to The Guardian, capacity expanded sharply between 2021 and 2025 and at certain points it has made up a noticeable share of the electricity mix. What stands out, though, is how this shift has come about. It hasn’t really been pushed by policy as much as it has been pulled by consumers themselves. Faced with rising costs and inconsistent supply, households and businesses have been looking for ways to regain some control over how they consume energy.

Yet, just as this transition began to gather pace, a series of policy changes introduced new hurdles. Import restrictions, additional taxation, and changes in net metering have altered the economics of solar adoption. For some, the return on investment has stretched further into the future. For others, the barrier to entry has moved even higher.

What makes this more striking is that other countries have taken a different approach. In several markets, once solar started gaining traction, taxes were reduced or removed to encourage adoption. In Pakistan, the cost has moved in the opposite direction, becoming harder to absorb at a time when demand is rising.

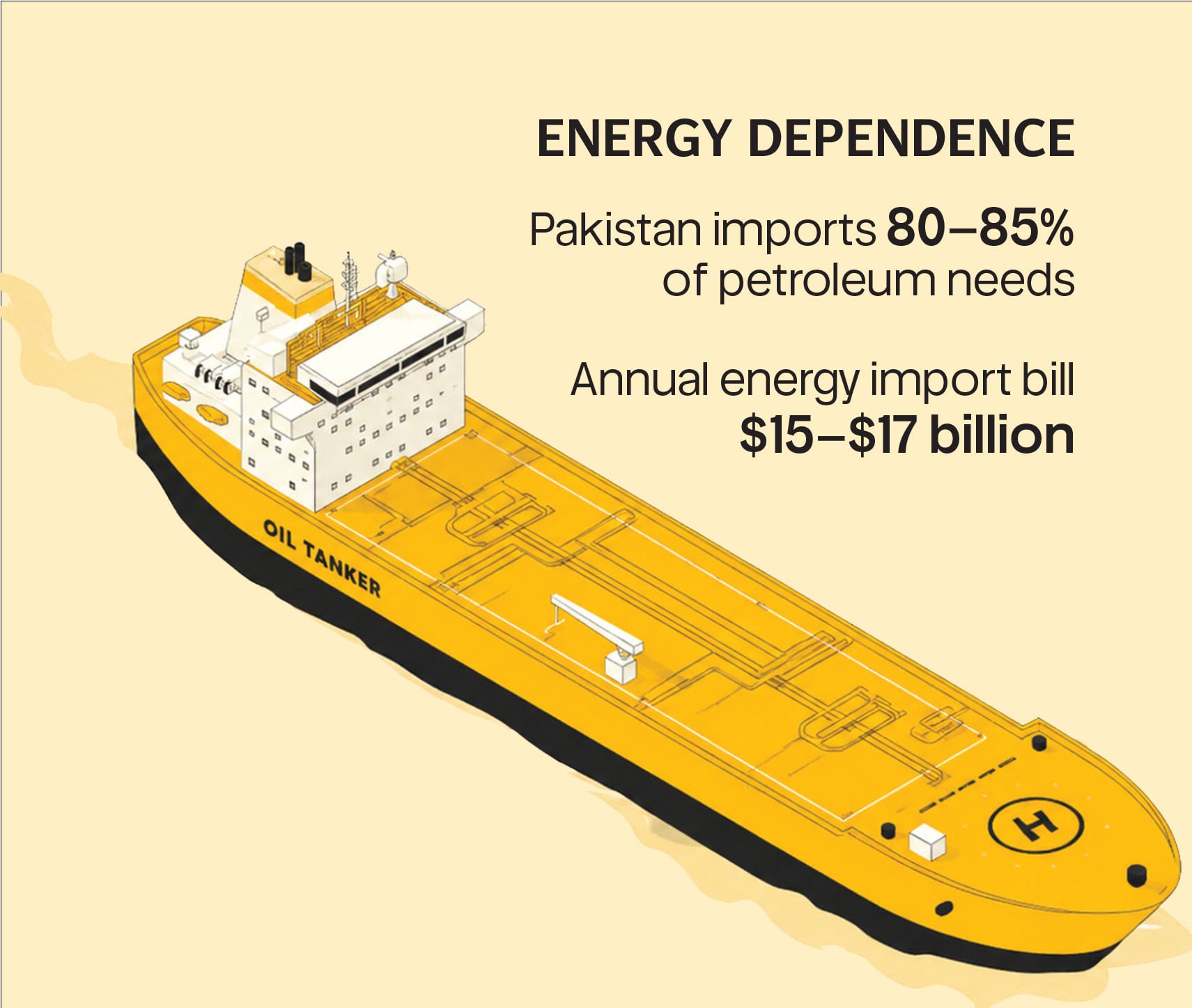

At the same time, relief has been hard to come by. Fuel prices have remained unpredictable, electricity bills have soared, and for most households the pressure has only grown. Even if global supply disruptions are far from Pakistan, their effects don’t stay that far. The country still depends heavily on imported fuel, so global shifts tend to show up here, one way or another.

On one side, more people are turning to solar to manage these pressures; on the other, the system has not quite kept pace — making the shift slower and more uneven than it could have been.

All of this brings up several obvious questions. If solar is picking up, why is Pakistan still so dependent on imported energy? What is actually stopping solar from moving beyond a certain point? And just as important, who is really benefiting from this shift, and who is still left out of it?

Import dependency

For all the talk of a shift toward solar, one thing has not really changed. Pakistan still runs on imported energy, and that dependence continues to shape how vulnerable the economy remains.

The country has made some progress in adding renewable sources to its energy mix, and solar has started to show up more visibly in recent data. But when placed against the overall system, the shift appears far more limited than it sometimes seems.

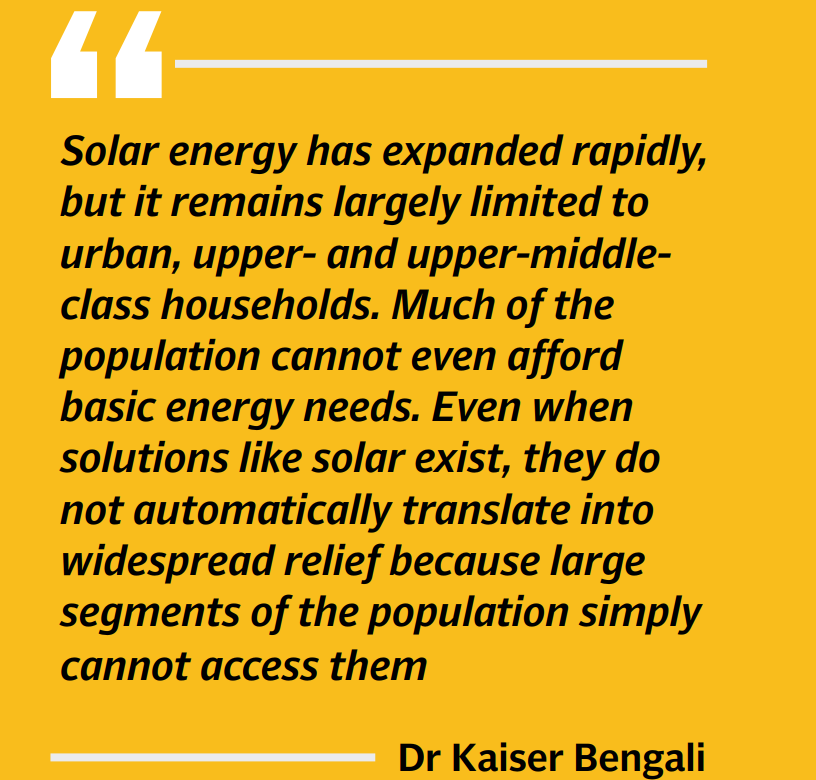

Dr Kaiser Bengali, an economist who has worked extensively on development and energy issues, believes the core problem has remained largely unchanged. “Over the past 25 to 30 years, our dependence on imports has steadily increased,” he said. “While renewable energy has grown slightly, its contribution is still minimal, almost negligible in the overall energy mix. Solar energy, for instance, remains largely limited to urban, upper- and upper-middle-class households.”

For him, the issue is not just about how much solar capacity has been added, but who is actually able to benefit from it. “Affordability is a major barrier. Many people cannot even afford basic energy needs. In such conditions, installing solar systems or backup power solutions is simply out of reach.”

This gap between availability and access is what keeps the broader structure intact. Even as a segment of consumers moves toward solar, the larger system continues to rely heavily on imported fuels. That also means external shocks, whether global price shifts or regional instability, still filter through fairly quickly.

Asked whether Pakistan can realistically reduce its fuel import bill in the next five to ten years, Bengali pointed to factors beyond domestic control. “It depends heavily on global conditions, especially geopolitical developments like conflicts in the Middle East,” he said. “However, our vulnerability stems from our own import dependence. If we relied less on imported fuels, external shocks would have a much smaller impact.”

A similar view emerges from Dr Khalid Waleed, a research fellow in energy economics at the Sustainable Development Policy Institute (SDPI), who sees the current transition as incomplete. “Pakistan’s ongoing shift toward solar energy is real, but it would be premature to call it fully structural,” he said. “What we are seeing is less a planned transition and more a market-driven adjustment to high tariffs, unreliable supply, and imported fuel volatility. In that sense, solar has emerged as a hedge rather than a coordinated policy outcome.”

That distinction becomes important when looking at the bigger picture. “The risk is not merely replacing one dependency with another, but creating a fragmented system where import dependence shifts from fuels to technologies such as panels, inverters, and storage systems, without building domestic industrial depth,” Waleed explained.

Even the policy environment, he argued, is shaped by deeper economic constraints. “With a power sector circular debt exceeding Rs2 trillion and fiscal space tightly constrained, policy decisions are often guided by short-term pressures rather than long-term system optimisation,” he said.

All that said, the dependence on imported fuel is showing no signs of fading completely. The structure of the power sector remains largely intact. Bengali believes this gap defines Pakistan’s current position. “Our vulnerability stems from our import dependence,” he cautioned, adding that if we relied less on imported fuels, external shocks would have a much smaller impact.

Taken together, these pressures point to a more complicated reality. Solar may be expanding, but it is being added onto a system that still relies heavily on imported fuels. Which then brings up another layer to this shift. If solar is growing at this pace, why does the system itself still look and operate the same way? Why does fossil fuel continue to dominate the broader mix, and what exactly has changed beneath the surface?

A system that refuses to shift

If solar is expanding as quickly as it appears, the expectation would be that the broader energy system would begin to shift with it. But that has not quite happened.

The most visible change has been at the consumer level, rooftops and small commercial setups across urban centres. Beneath that, however, the structure of the system has remained largely the same.

According to Dr Kaleem Ullah, Associate Professor at the US-Pakistan Center for Advanced Studies in Energy (USPCAS-E) at the University of Engineering and Technology, Lahore, the core architecture of Pakistan’s power system has not really shifted despite the rise in solar adoption.

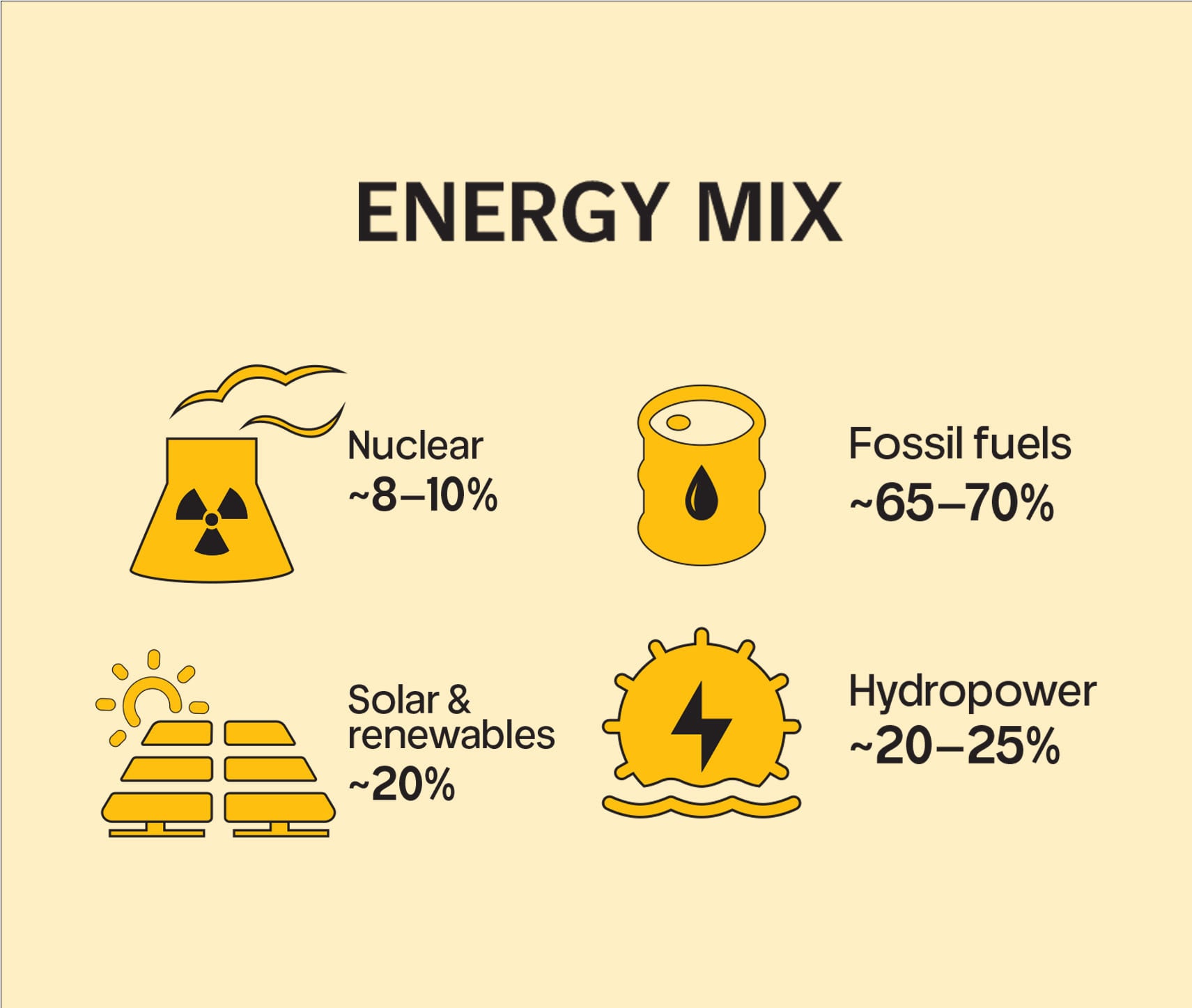

“The most important unchanged feature is that Pakistan still runs on a centralised, fossil-heavy, capacity-payment-based power system,” he said. “As of March 2025, thermal power still made up about 55.7 per cent of installed capacity, and remained the single largest block in actual generation as well.”

Alongside that is a set of structural issues that have persisted for years. “Transmission and distribution losses remain extremely high, circular debt has climbed to around Rs2.39 trillion, and the system is operating at barely a third of its installed capacity,” he explained. “So solar has grown, but the basic architecture has not yet been transformed.”

This gap between visible growth and underlying change is where much of the confusion around the solar transition begins. At one level, more solar capacity should reduce reliance on fossil fuels. In practice, the system still leans heavily on them, and for reasons that go beyond electricity alone.

“Fossil fuel dominance persists for three reasons: legacy assets, system operations, and end-use dependence,” Kaleem said. “The grid still needs dispatchable power for evening peaks, and beyond electricity, the wider energy economy continues to run on oil, gas, and coal.”

That distinction matters. Even if solar expands within the power sector, large parts of the economy, transport, industry, and household energy use, remain tied to conventional fuels.

“The hardest sectors to transition are transport, heavy industry, and residential gas use,” he said. “Solar can replace daytime electricity relatively quickly, but it cannot easily replace diesel for transport or gas for household demand.”

In that sense, the shift toward solar is happening, but within limits set by a system built around a very different set of assumptions.

Which brings the focus back to a deeper question. If solar is clearly picking up, but the system itself has not shifted with it, then what is actually slowing this transition down? Where does the bottleneck lie, in cost, policy, or the structure of the system itself?

Transition helps, not fixes

For many households and businesses, the benefits of solar are already visible. Lower daytime electricity bills, some protection from tariff increases, and a degree of independence from an unreliable grid have made it an increasingly practical option.

But beyond that immediate relief, the picture begins to change. According to Kaleem Ullah, the way solar is often discussed in Pakistan tends to blur an important distinction between individual benefit and system-wide impact.

“Yes, but only if energy security is being looked at too narrowly,” he said. “Solar improves resilience for households and firms by lowering daytime electricity costs and reducing exposure to tariff shocks.”

That improvement, however, operates within a limited window. “At the system level, solar alone does not solve evening peak demand, grid instability, circular debt, transmission congestion, or fossil dependence in transport and industry.”

This gap between what solar can do at the consumer level and what it cannot do at the system level is where expectations begin to diverge. A growing share of electricity during the day may come from solar, but the grid still has to meet demand after sunset and support sectors tied to conventional fuels.

“Higher shares of solar and wind are achievable,” Kaleem noted, “but only with investment in transmission, system flexibility, forecasting, operational reforms, and storage.”

Even then, deeper financial pressures remain. “More renewable energy does not, by itself, reduce the capacity charges tied to existing conventional plants,” he said.

Taken together, this suggests that solar is doing what it is meant to do, but within limits that are often overlooked. It is helping consumers manage costs, but it is not, on its own, fixing the deeper structural issues of the energy system.

Which then leads to the next question: what exactly is preventing this transition from moving beyond these constraints?

Growth exists, but scale does not

If solar is growing, and if its benefits at the household level are already visible, the obvious question is why that growth has not translated into a wider shift.

The answer does not sit in one place. It runs through policy, pricing, and the way the system itself is structured.

For Waleed, Research Fellow in energy economics at SDPI, the problem is less about the absence of policy and more about the contradictions within it.

“The regulatory barriers are less about absence of policy and more about conflicting objectives,” he said. “On one hand, there is a desire to promote renewable energy, and on the other, there is a need to safeguard the revenues of distribution companies and service long-term power purchase agreements.”

That tension explains why policy around solar has often appeared inconsistent. “Every incremental unit of rooftop solar reduces demand from the grid,” Waleed said. “That, in turn, raises per-unit costs because of fixed capacity payments. This feedback loop creates resistance within the system and leads to periodic policy reversals. In essence, solar is both a solution and a stress test for an already strained power sector.”

The result is a transition that moves forward, but unevenly. “Solar adoption is disproportionately concentrated among middle- and upper-income households, while lower-income consumers remain locked into an increasingly expensive grid,” he added.

That unevenness is also visible on the ground. According to Waqas Moosa, the market has seen strong growth, but not in a steady or consistent way.

“There was a dip, and part of that goes back to policy decisions,” he said. “When imports were restricted around mid-2022, the supply chain was disrupted. What we saw in 2023 and 2024 was not just normal growth, it was almost two years of demand coming into one.”

Since then, the market has begun to settle. “The market is still growing, but at a slower, more natural pace,” he said. “That tells you the demand is there, but it is being shaped by constraints.”

Those constraints are most visible when it comes to cost. “You are looking at around 18 per cent tax on most components,” Moosa said. “A system that should cost around one million ends up closer to 1.2 million. That alone makes a difference for many households.”

Even where steps are being taken to ease the process, their impact appears limited. According to Waqas Moosa, the recent decision to remove licensing fees does little to address the core bottlenecks.

“The fee was a small percentage of the total cost,” he said. “The more important issue is that application processing needs to be devolved from NEPRA to the DISCOs. Adding an extra approval step creates at least a month’s delay.”

He pointed out that this is not a new issue. “The original 2015 net metering regulations had the same problem. It was later shifted to DISCOs because of delays, and now the same mistake is being repeated.”

Financing remains another barrier. “Solar is a high-value purchase, and you need financing to make it accessible,” he said. “Right now, that support is very limited, especially for middle-income households and SMEs.”

Put together, the picture becomes clearer. The demand for solar exists. The technology is available. The economic logic, in many cases, still holds.

Which brings us to the real question: demand and benefits are clear, so why is the system itself still holding the transition back?

The system is not ready

If the barriers to solar adoption appear visible at the policy and market level, a deeper constraint lies within the system itself. Even where solar is growing, the system it feeds into has not been designed to fully accommodate it.

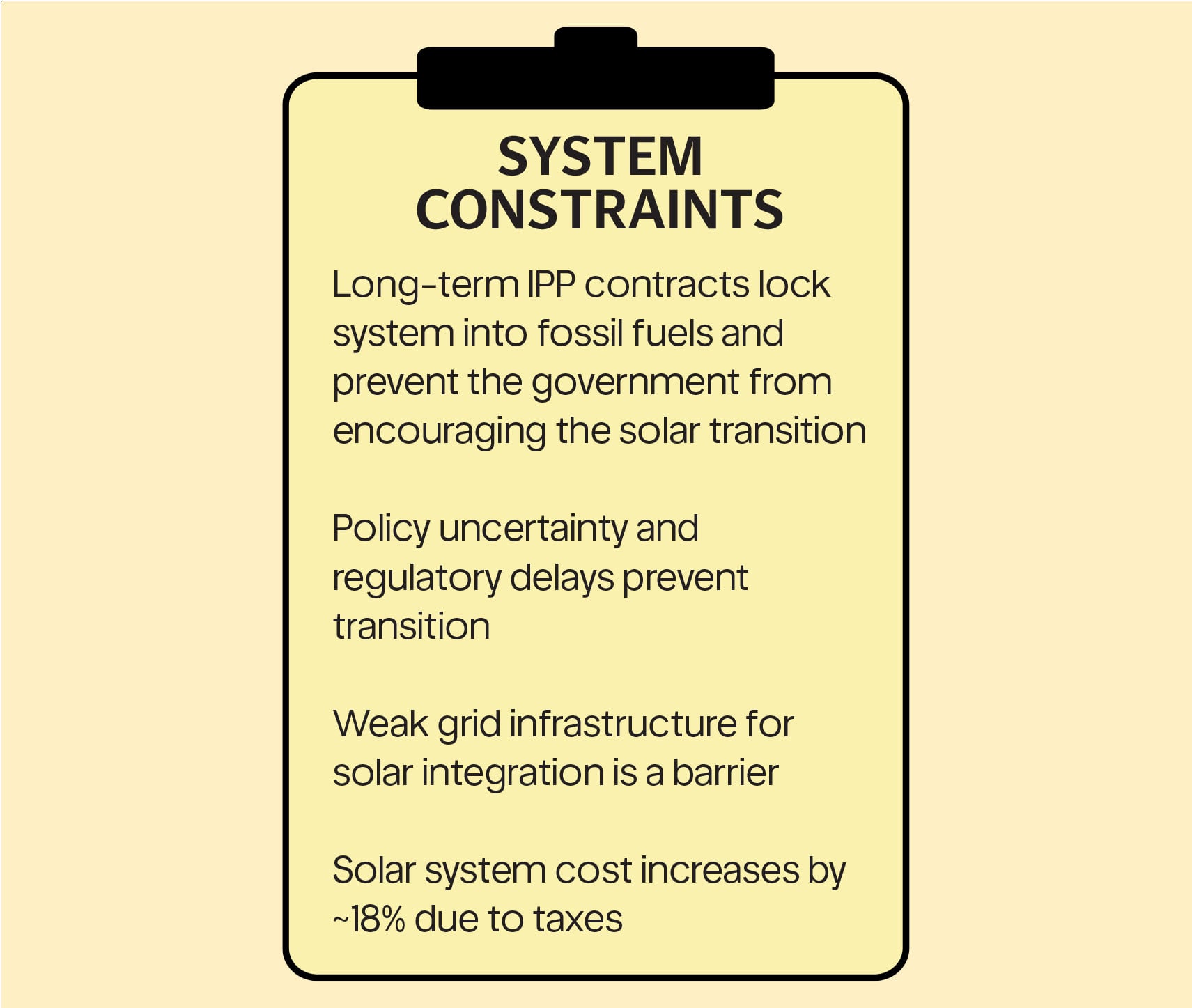

One of the clearest examples of this comes from the way Pakistan’s power sector is structured around long-term contracts.

According to Kaleem Ullah, legacy Independent Power Producer (IPP) contracts remain one of the biggest constraints on any meaningful transition.

“Many of these agreements were built around dollar indexation, guaranteed returns, and capacity payments that must be made whether electricity is used or not,” he said. “So even if solar reduces the cost of electricity during the day, it does not remove the fixed financial burden of those contracts.”

That burden is significant. “Capacity payments have reached into the trillions of rupees, and consumers are effectively paying for a large share of electricity that is never used,” he explained. “What you have is a system where cheap solar is being added on top of an already expensive structure, without reducing the underlying cost pressures.”

That creates a situation where the system, rather than adapting to solar, has an incentive to resist it.

But contracts are only one part of the challenge. The physical infrastructure of the grid presents another. “The biggest bottleneck is not the availability of sunlight,” Kaleem said. “It is the ability of the grid to absorb, move, and balance that power efficiently.”

Transmission constraints, weak distribution networks, and slow system upgrades limit how much solar can actually be integrated. “This is why solar can grow quickly at the consumer level, but still be difficult to integrate at a national scale,” he said. “The network has not kept pace.”

These limitations are not just technical, they are also financial. According to Waleed, the same constraints that shape policy decisions also limit the system’s ability to adapt.

“Financial constraints operate at multiple levels,” he said. “For households, upfront capital costs remain a barrier. But at the state level, limited fiscal space restricts investment in transmission upgrades, grid flexibility, and storage.”

“You end up with a shift that is happening organically, driven by consumers, but without the institutional and infrastructure support needed to sustain it at scale,” he added.

Taken together, the challenge isn’t just adding solar capacity – it’s whether the system can absorb that growth in a way that genuinely changes how energy is produced and delivered. That raises another question: if the system itself isn’t fully aligned with the transition, who actually benefits, and who remains locked out?

Who benefits from solar?

As solar continues to expand, another question begins to surface, one that is less about capacity and more about access.

Who is actually benefiting from this shift? At first glance, the answer seems straightforward. The most visible adopters have been households and businesses that can afford the upfront cost.

But according to Moosa, looking at the transition only through that lens can be misleading. “When any new technology comes in, it is always the more affluent who adopt it first,” he said. “The real question is not who is benefiting right now, but how that benefit spreads over time.”

For him, the more useful way to understand solar is through its impact rather than its initial distribution. “The impact is very different depending on who you are looking at,” he explained. “For some, it is about saving money. But for others, especially those with limited or unreliable access to electricity, it can change daily life, from being able to study at night to storing food properly.”

Yet, despite that potential, access remains uneven. According to Waleed, the way the current system is evolving risks reinforcing those differences rather than reducing them.

“Solar adoption is disproportionately concentrated among middle- and upper-income households, while lower-income consumers remain locked into an increasingly expensive grid,” he said.

That dynamic also shifts how costs are distributed. “As more consumers move toward solar, those who remain on the grid end up bearing a larger share of fixed system costs,” he explained, raising questions around energy equity.

There is also a longer-term concern about how this trend could evolve. Moosa pointed to what is often described as a “utility spiral”, where more financially capable consumers gradually move away from the grid, leaving a smaller base to absorb the same costs.

“When people start moving off the grid, the costs do not disappear,” he said. “They get redistributed among those who are left, and as that group shrinks, the burden increases.”

If that cycle continues, the most vulnerable consumers risk being left with a disproportionate share of the cost.

That is where the conversation around solar moves beyond technology and into questions of access and design. Because while the transition is underway, it is not unfolding evenly.

For some, solar offers savings and flexibility. For others, it remains out of reach.

And that uneven shift raises a broader question. If the transition is not inclusive by default, then what would it take to make it so?

Fix the system before scaling solar

By this point, the direction of the problem becomes clearer. Solar is not lacking momentum. The demand exists, the technology is available, and the economic case, at least for some consumers, is already visible. What is missing is alignment.

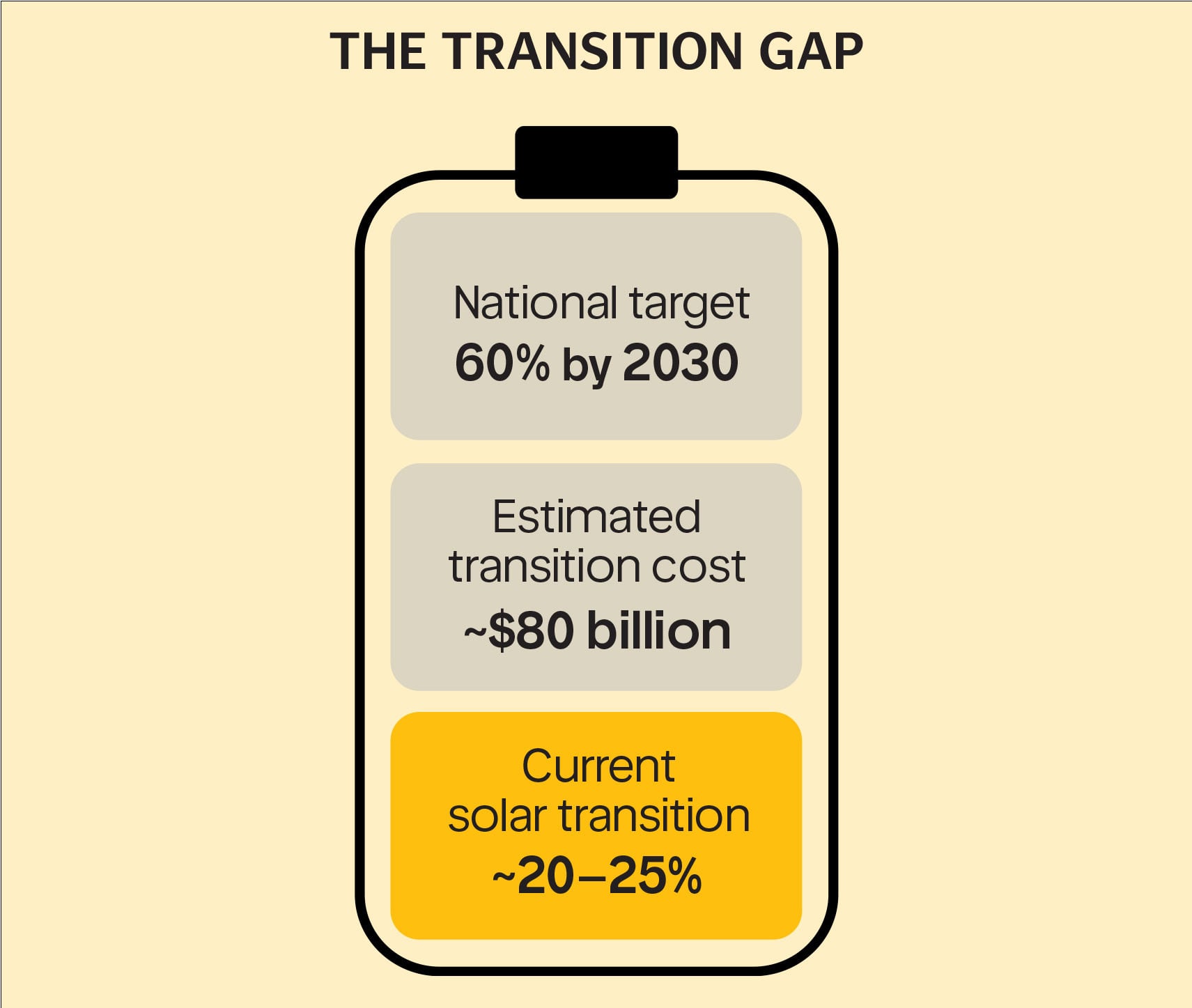

For Dr Khalid Waleed, the next phase of the transition cannot be approached in the same way as the last. “Moving toward a 50 to 60 per cent renewable energy share would require a fundamental shift in planning philosophy,” he said. “The priority is no longer adding generation capacity, but enhancing system flexibility.”

That means focusing on the basics. “This includes large-scale deployment of battery storage, modernisation of the transmission network, and digitalisation of grid operations,” he said, adding that the more difficult part lies in addressing the legacy system itself. “It also requires confronting the issue of underutilised thermal assets.”

This is where capacity rationalisation becomes critical. “Early retirement of inefficient plants, or repurposing them into grid-support infrastructure, can create space for renewables while also reducing capacity payments,” he said. “Without that, the system remains financially and operationally constrained.”

Even then, the path ahead is not straightforward. “Under current conditions, Pakistan’s renewable targets remain aspirational,” Waleed noted. “Solar will continue to grow, but increasingly alongside storage, as consumers look for more reliable solutions.”

For Dr Kaleem Ullah, the barriers to that transition are already well known. “Grid weakness, legacy thermal contracts, financial stress, and policy inconsistency all play a role,” he said. “Even if solar becomes cheaper, the system around it is not yet flexible enough to support large-scale integration.”

That limitation defines how far the transition can realistically go. “Pakistan can make solar much larger,” he said, “but it cannot turn it into the dominant solution without first fixing the institutions and infrastructure underneath the power system.”

Alongside these structural changes, there are more immediate ways to make solar’s benefits more widely accessible. According to Waqas Moosa, part of the solution lies in how those gains are distributed.

“One way is to pass on the benefit of cheaper daytime electricity to everyone,” he said. “If solar is lowering costs during certain hours, that should be reflected in tariffs so that even those who do not have solar can benefit from it.”

Taken together, these ideas point in the same direction. The question is no longer whether solar will continue to grow. It almost certainly will.

The real question is whether the system around it can evolve quickly enough to make that growth meaningful, not just for a segment of consumers, but across the broader economy.